As the global shift toward real-time digital tax compliance accelerates, the United Arab Emirates is taking a bold step forward with the rollout of a national e-invoicing framework. At the heart of this transformation is PEPPOL a globally recognized standard for structured and secure electronic document exchange.

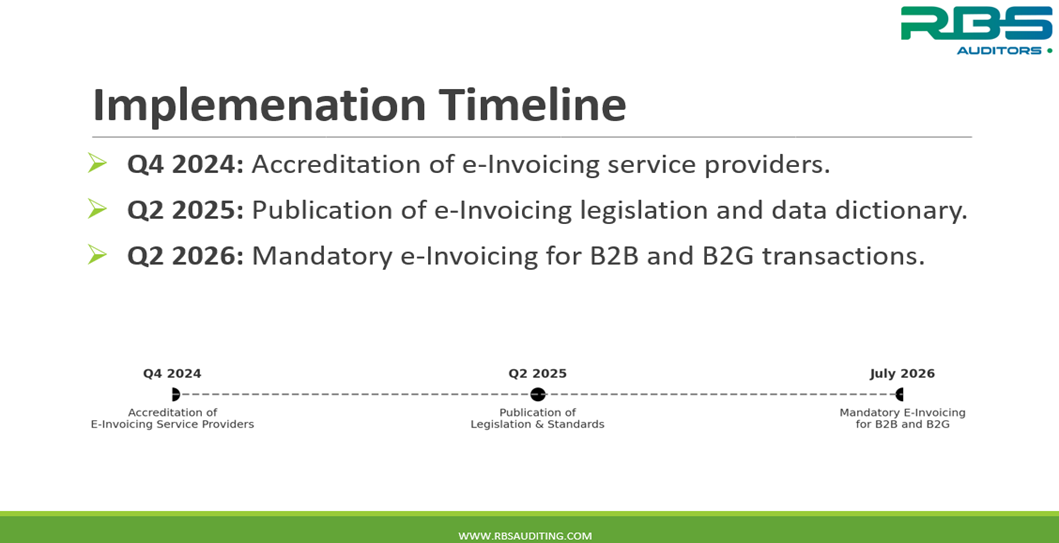

In alignment with international best practices and the UAE’s commitment to innovation and transparency, the Digital Continuous Transaction Controls and Exchange (DCTCE) model will redefine how businesses issue, report, and receive invoices. With full implementation expected by July 2026, this initiative marks a major milestone in the country’s digital tax journey, enhancing both compliance and operational efficiency across sectors.

In this article, we explore the PEPPOL network, the PINT AE standard, the five-corner model, and the critical steps UAE businesses must take to prepare for this new era of tax digitization.

As of now (July 2025), the United Arab Emirates (UAE) is in the process of implementing e-invoicing, aligning with global digital transformation trends and the practices of neighboring Gulf countries like Saudi Arabia, which already has a mature e-invoicing system.

Here’s what UAE businesses should know:

What is E-Invoicing?

E-Invoicing is an integrated and structured form of invoice data that is issued and exchanged electronically between a supplier and a buyer and reported electronically to the UAE Federal Tax Authority. It replaces traditional paper or PDF invoices.

UAE E-Invoicing Status (as of mid-2025)

- The UAE Federal Tax Authority (FTA) has not yet made e-invoicing mandatory, but it is expected to introduce it soon, especially for VAT-registered businesses.

- Pilot programs or voluntary e-invoicing initiatives may already be underway (especially for large enterprises or B2G transactions).

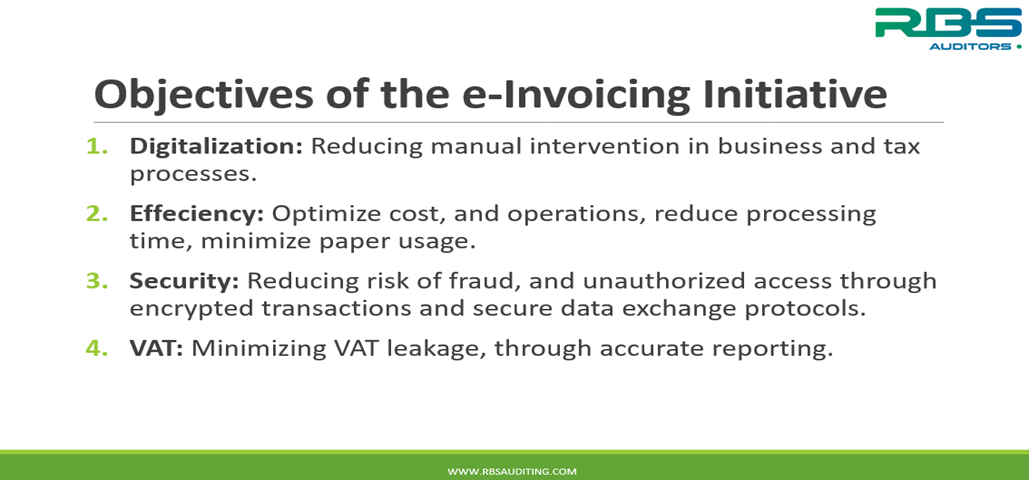

Objectives of The e-invoicing Initiative

Implementation-Timeline

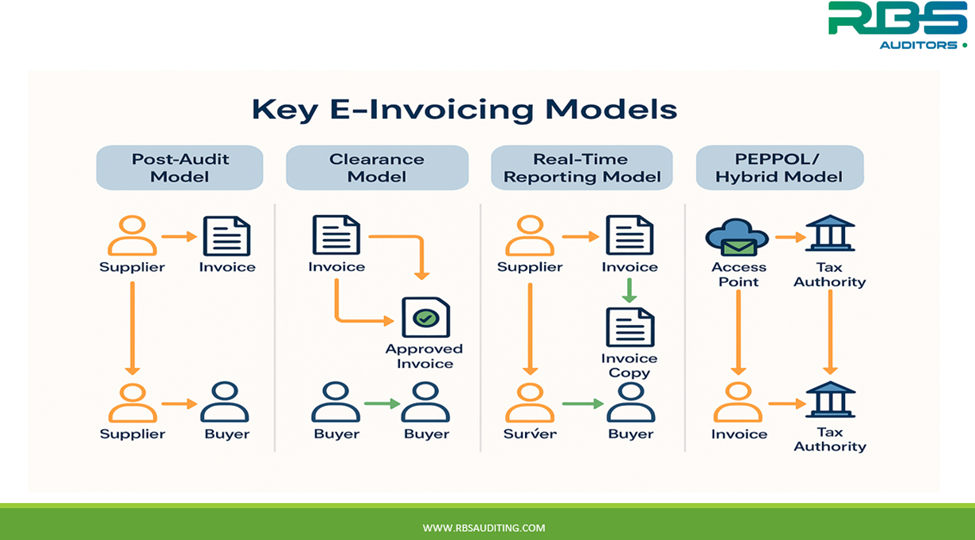

Key E-Invoicing Models Explained

1. Post-Audit E-Invoicing Model

The Post-Audit Model is the traditional and least intrusive form of e-invoicing, where invoices are exchanged directly between the supplier and buyer without prior validation by the tax authority. Under this model, the tax authority audits invoices retrospectively, usually during periodic tax filings or formal audits.

This system relies on businesses to generate, transmit, and archive invoices according to legal standards. Tax authorities may request access to records during inspections to verify VAT compliance, detect fraud, or assess liabilities.

Key Features

- No real-time interaction with tax authorities

- High flexibility in invoice format and transmission methods

- Requires robust archiving and audit trail mechanisms

Examples

- United States

- Germany (transitioning to clearance by 2025)

- Japan

- Canada

2. Clearance E-Invoicing Model

The Clearance Model is a real-time, government-controlled e-invoicing system, where each invoice must be validated or “cleared” by the tax authority before it is sent to the buyer. This model ensures that all taxable transactions are visible to the government at the point of issuance, significantly reducing the risk of tax fraud, especially related to VAT evasion and fake invoices.

In a clearance setup, the invoice is either routed through a centralized platform (e.g., India’s IRP, Mexico’s SAT, Saudi Arabia’s ZATCA) or integrated directly with government APIs. The system assigns a unique code or timestamp, certifying the invoice as legally valid.

Key Features

- Invoice must be submitted to and cleared by the tax authority before it is valid

- Real-time or near-real-time approval

- Often requires specific structured formats (e.g., XML, JSON)

- Typically involves QR codes, digital signatures, or UUIDs

Examples

- Mexico (CFDI)

- India (IRP system for GST)

- Saudi Arabia (ZATCA e-invoicing)

- Turkey, Vietnam, Chile

3. Real-Time Reporting (RTR) E-Invoicing Model

The Real-Time Reporting (RTR) Model allows businesses to exchange invoices directly with their trading partners, while simultaneously or shortly after, a copy of the invoice is sent to the tax authority for monitoring. Unlike the clearance model, tax authorities do not approve the invoice before transmission, but they receive data almost immediately.

This model strikes a balance between business flexibility and regulatory oversight, enabling governments to monitor transactions in near real-time without disrupting invoice flows.

Key Features

- Invoice sent to buyer without prior tax authority approval

- A digital copy is transmitted to the tax authority in real-time or within a mandated window (e.g., 4 days)

- Often integrated directly into ERP or invoicing systems

- Focus on data transparency, not clearance control

Examples

- Spain (SII system)

- Hungary

- Italy (for e-receipts and certain sectors)

- Portugal (SAF-T & real-time transmission for some industries)

4. PEPPOL / Hybrid Exchange E-Invoicing Model

The PEPPOL (Pan-European Public Procurement Online) / Hybrid Exchange Model is a network-based e-invoicing framework designed to enable secure, standardized, and interoperable exchange of electronic documents mainly between businesses and governments (B2G), but increasingly for B2B use as well.

In this model, invoices are transmitted through certified Access Points (APs) using the PEPPOL BIS (Business Interoperability Specifications) format, typically based on UBL (Universal Business Language) standards. It enables cross-border invoicing and ensures that all parties in the network “speak the same digital language.”

Key Features

- Uses a four-corner model: supplier AP → buyer AP

- Standardized formats (e.g., PEPPOL BIS 3.0, UBL XML)

- Focus on interoperability and compliance across regions

- Can coexist with clearance or RTR models (hence “hybrid”)

Examples

- European Union (mandatory for B2G in most countries)

- Singapore, Australia, New Zealand (PEPPOL Authority)

- Japan, Malaysia (voluntary or pilot phases)

Key e-Invoicing Models

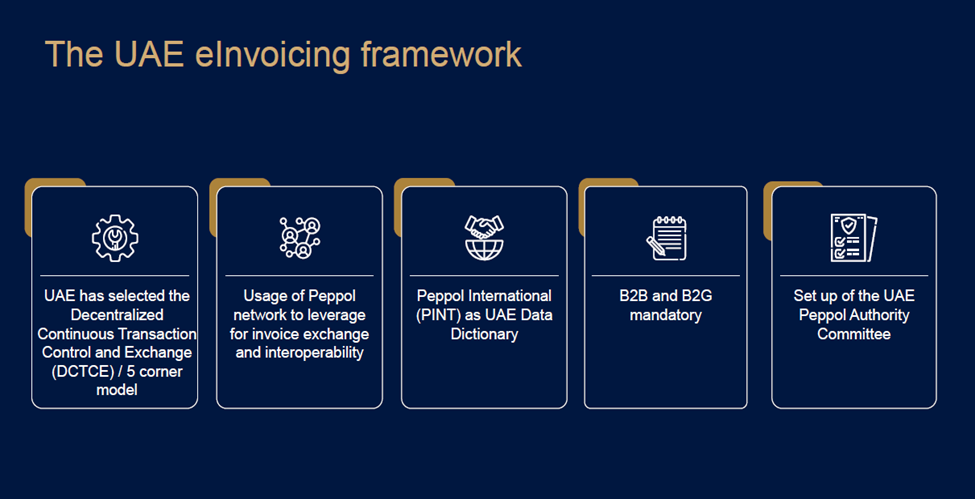

The UAE e-invoicing Framework

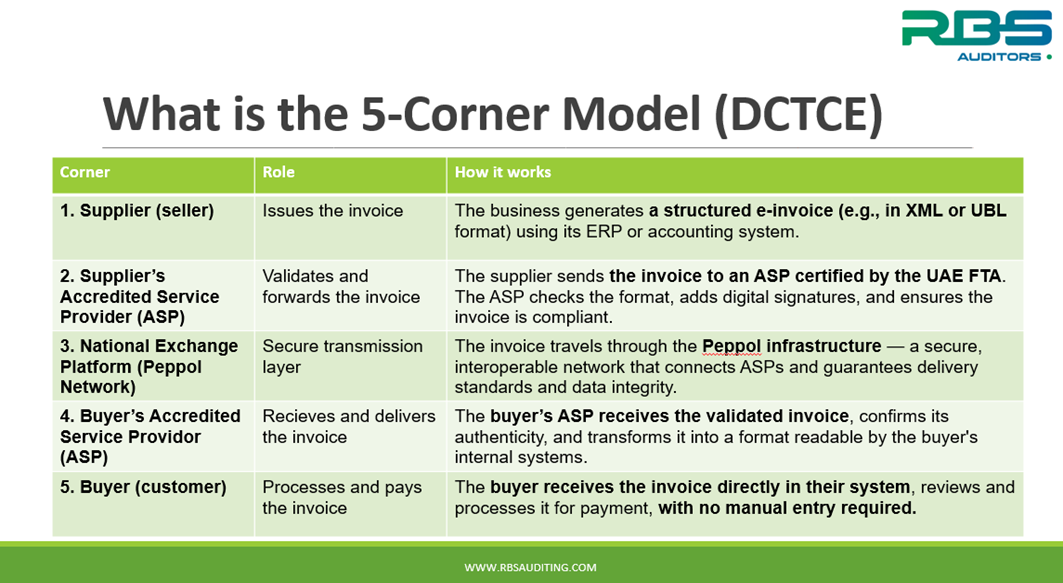

What is 5-Corner Model in E-Invoicing – DCTCE Model

The 5-corner model, also known as the DCTCE model (short for Digital, Clearance, Transmission, Compliance, and Exchange), is a conceptual e-invoicing framework under evaluation or design in jurisdictions like the United Arab Emirates (UAE) to support future corporate tax enforcement and digital transformation.

This model builds upon the more common 4-corner model (e.g., PEPPOL), by adding a fifth “corner”: the tax authority or central platform for real-time clearance or reporting.

Key Features of 5-Corner Model

- Digital-first: Fully digital invoice generation and exchange.

- Clearance & Compliance: Invoices must be approved or cleared through the tax authority before reaching the buyer.

- Audit Trail: Full traceability and archiving built into the workflow.

- Interoperability: Based on structured formats (e.g., XML, UBL).

- Real-time or near real-time data flow to the tax authority.

What is the 5-Corner Model (DCTCE)

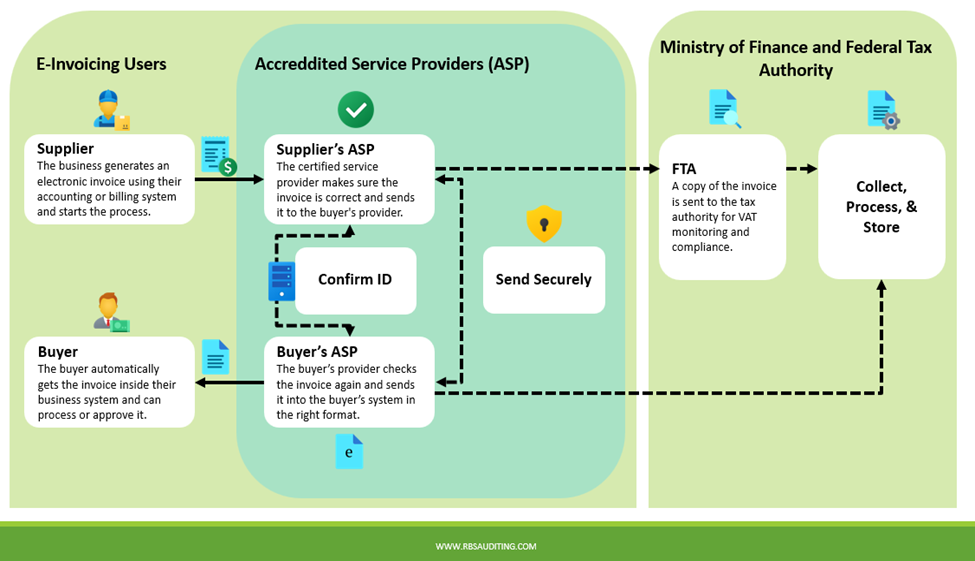

E-invoicing Process

What is PEPPOL Network?

PEPPOL (Pan-European Public Procurement Online) is an international eDelivery network designed to standardize and simplify the exchange of electronic documents, particularly e-invoicing, between businesses and governments (B2G) and increasingly between businesses (B2B).

Key Components of PEPPOL Network:

- PEPPOL BIS (Business Interoperability Specifications): Standardized XML formats for documents like invoices, orders, and credit notes.

- PEPPOL Access Points (APs): Certified intermediaries that send and receive documents within the network. Any PEPPOL-enabled organization can communicate with any other via their APs no need for custom integrations.

- PEPPOL SMP (Service Metadata Publisher): A directory that stores participant capability and addressing information, enabling automated document routing.

- PEPPOL Directory (or PEPPOL ID Registry): A searchable public directory of all organizations using PEPPOL, identified by a unique PEPPOL ID (like a digital address).

What is PINT AE?

PINT AE stands for “Peppol Invoice Notification Template – United Arab Emirates”, and it refers to the UAE-specific standard for electronic invoicing (e-invoicing) based on the Peppol BIS (Business Interoperability Specifications) framework.

Explanation

- PINT: A global initiative developed by OpenPeppol to localize Peppol standards for different countries (e.g., PINT SG for Singapore, PINT NO for Norway).

- AE: The ISO country code for the United Arab Emirates.

- PINT AE: Is the UAE’s customized implementation of the global Peppol e-invoicing format to ensure compatibility with the UAE’s tax laws, invoice fields, and regulatory requirements, particularly in the context of VAT and Corporate Tax.

What Does PINT AE Include?

XML-Based Invoice Structure

- A standardized e-invoice format based on UBL 2.1 XML schema that ensures structured and machine-readable invoice data.

Mandatory Data Elements

- UAE VAT number (TRN) for buyer and seller

- Invoice UUID (globally unique ID)

- Tax breakdown per line item

- Grand total (tax-inclusive)

- Digital signature fields (planned)

- QR code (in some cases)

Localization Rules

- Compliance with FTA guidelines and invoice retention laws

- Fields like Emirate name, Arabic text support, and local time stamps

- Support for dual-language invoicing (Arabic & English)

Validation & Compliance

- Documents must pass Peppol validation rules tailored for the UAE

- Only Accredited Service Providers (ASPs) certified under the UAE’s National E-Invoicing Program can transmit PINT AE documents.

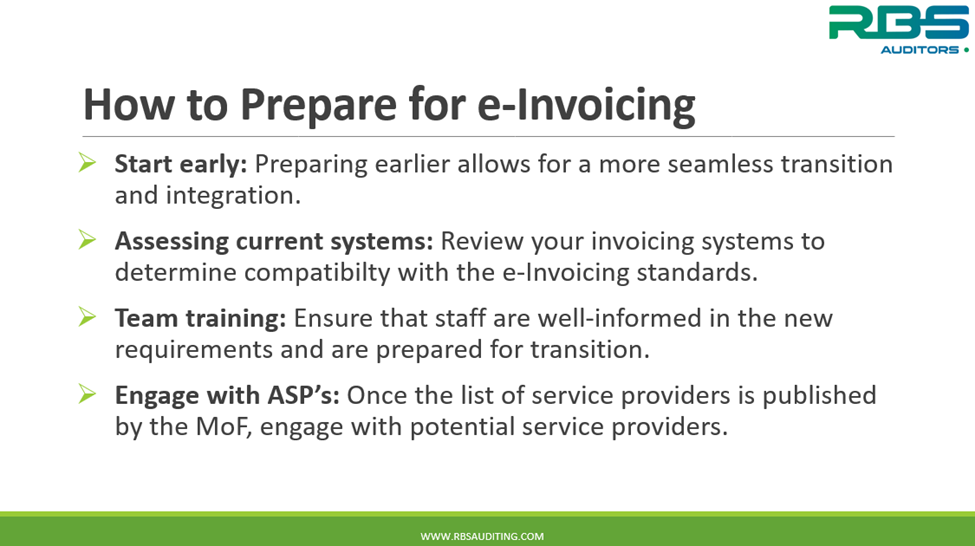

What You Should Do Now

If you’re running a business in the UAE

How to Prepare for e-invoicing

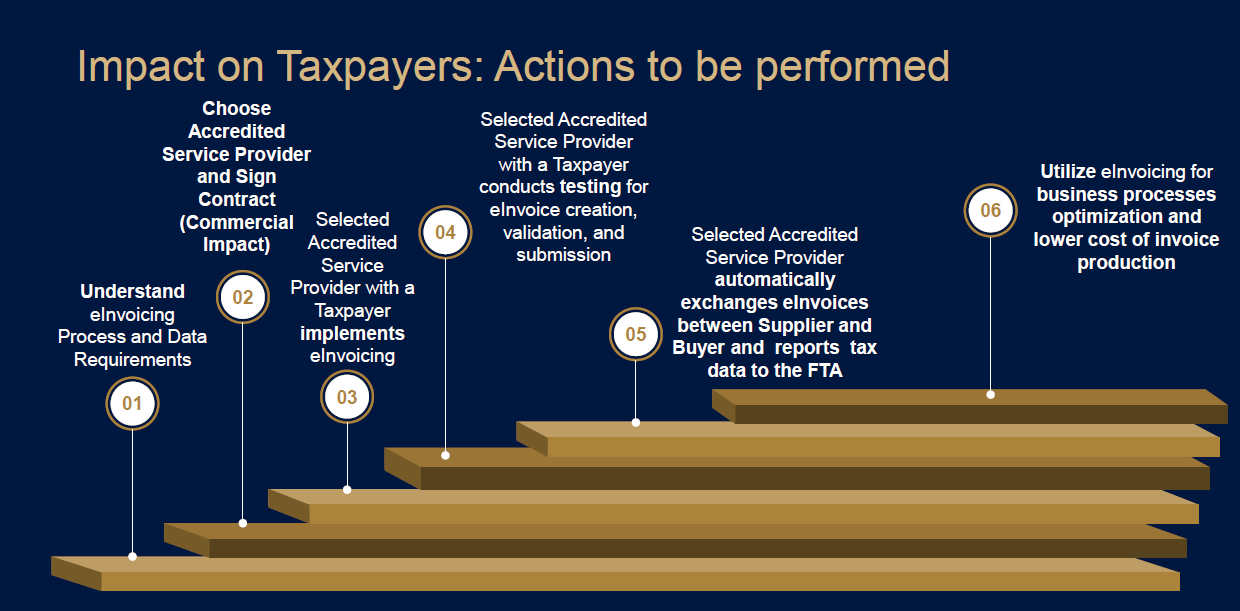

Impact on Taxpayers Actions to be Performed

Conclusion

The UAE’s move toward a nationwide e-invoicing system marks a bold and transformative step in aligning with global digital tax frameworks. By adopting a PEPPOL-based 5-corner model under the DCTCE (Digital, Clearance, Transmission, Compliance, and Exchange) framework, the UAE is not only enhancing tax transparency and compliance but also laying the groundwork for a more digitally integrated and efficient economy.

As the July 2026 rollout approaches, businesses across all sectors must begin preparing for this shift by upgrading their ERP systems, integrating with certified Accredited Service Providers (ASPs), and aligning their invoicing processes with the PINT AE standards.