In the UAE, the VAT treatment of selling commercial property depends on the type of sale and whether it qualifies for specific exceptions, such as the Transfer of a Going Concern (TOGC). Here’s an overview of the tax implications of selling commercial property in the UAE under the VAT rules (Federal Decree-Law No. 8 of 2017 on VAT and its amendments).

🏢 1. Sale of Commercial Property – Standard Case

✅ Tax Treatment: Subject to 5% VAT

- The sale of commercial property is generally taxable at the standard VAT rate of 5%.

- The seller is responsible for charging and collecting VAT from the buyer.

- This applies whether the property is:

- Completed and leased

- Vacant

- Sold to a taxable or non-taxable person

💡 Exceptions

If the transaction qualifies as a TOGC, VAT does not apply (see next section).

The sale of residential property is treated differently—the first supply may be zero-rated, and subsequent supplies may be exempt.

🔄 2. Transfer of a Going Concern (TOGC)

✅ Tax Treatment: Outside the Scope of VAT

If the commercial property is sold as part of a business transfer, and certain conditions are met, the sale may be treated as a TOGC, and no VAT is charged.

TOGC Requirements (as per UAE VAT Law & FTA guidance):

⚠️ Important

If only the property is sold, and not the business, TOGC does not apply.

For example, the sale of property without continuing the lease or property is used for their own business purpose, then TOGC does not apply.

Proper documentation is required to support TOGC treatment in case of an audit.

📉 3. Input VAT Recovery

Buyers who are VAT-registered may be able to recover the input VAT paid on the purchase (via their VAT return), provided the property is used to make taxable supplies (e.g., renting to businesses).

Non-registered buyers or those using the property for VAT-exempt purposes (e.g., non-commercial use) cannot claim input VAT.

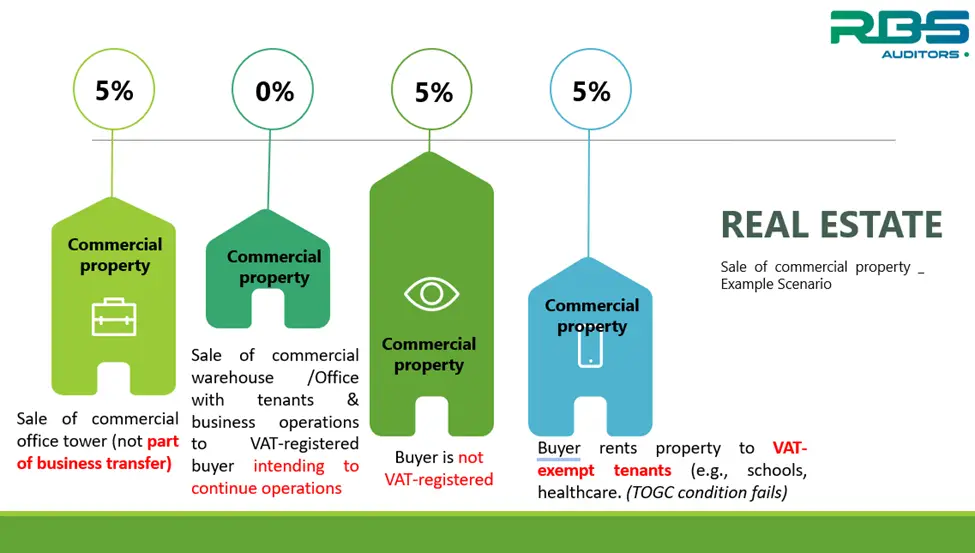

✅Example: Case Scenario

🚫 Problem: When Buyer Rents to VAT-Exempt Tenants:

If the buyer does not intend to make taxable supplies (because their tenants are VAT-exempt and they will not charge VAT on rent), then:

The buyer cannot recover input VAT on related costs (e.g., legal fees, refurbishments).

FTA may disallow TOGC treatment because one condition of TOGC is that the buyer must continue the same business of making taxable supplies.

If TOGC treatment fails, the seller must charge VAT on the sale.

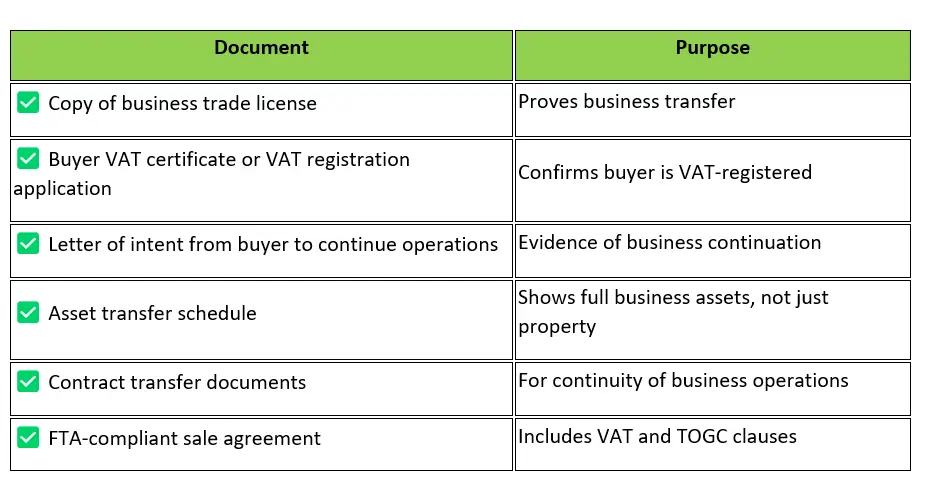

🧾 Supporting Documentation Checklist

To safely apply TOGC treatment and protect both parties from future VAT assessments or penalties:

⚠️ Risks if Not Properly Documented

If TOGC is incorrectly applied, FTA may assess 5% VAT + penalties + interest on the seller.

The buyer may be unable to recover VAT if the invoice is missing or the conditions aren’t met.

FTA audits often require proof of business continuation and the buyer’s VAT status at the time of transfer.

🧾Summary – TOGC

Reference

📘 1. Federal Decree‑Law No. 8 of 2017 on VAT – Article 7(2)

Under Article 7(2), the transfer of a whole business (or part capable of separate operation) from one person to a taxable person intending to continue the business is not treated as a supply for VAT purposes, and therefore outside the scope of VAT.

📝 2. FTA Public Clarification VATP015 (20 August 2019)

FTA clarified the three conditions for TOGC treatment:

1. Transfer of a whole or independent part of a business (including assets, premises, contracts, employees)

2. Transfer to a taxable person (whether already registered or having a pending/accepted VAT registration)

3. The buyer intends to continue the same kind of business. This clarification confirms that Article 7(2) is mandatory and that TOGC is outside the VAT scope if the conditions are met.

✅ Conclusion: Use TOGC to Close Smarter, Not Costlier

Avoiding unnecessary VAT costs in a commercial property transaction is not just possible—it’s entirely legal if you understand and apply the TOGC rules correctly. Whether you’re a property developer, investor, or advisor, recognizing when a sale qualifies as a Transfer of a Going Concern can have a significant impact on the deal’s bottom line.

💼 Before signing, consult your legal and tax advisors to ensure all three conditions of TOGC are met—and properly documented. It’s a small step that can save millions in VAT.

If you found this article useful, please like, share, and subscribe for more expert insights on UAE tax law, real estate transactions, and VAT compliance strategies. Got questions or a real-life scenario? Drop them in the comments—we’re here to help you navigate VAT with clarity and confidence.

🎓 Want to Learn More?

If you’re ready to deepen your understanding of UAE CT law, including how to structure, manage compliance, and avoid costly errors, check out our comprehensive UAE Corporate Tax online course.

👉 Explore the Course on Our RBS LearnWorlds Platform. Whether you’re a professional, an accountant, or a business owner, this course is designed to give you practical, actionable knowledge—no legal jargon, just clear guidance.

📚 Enroll today and gain the confidence to handle UAE CT Law in complex transactions like a pro. https://rbsauditors.learnworlds.com/